This blog is a preview of our State of Web3 Report. Sign up here to download your copy!

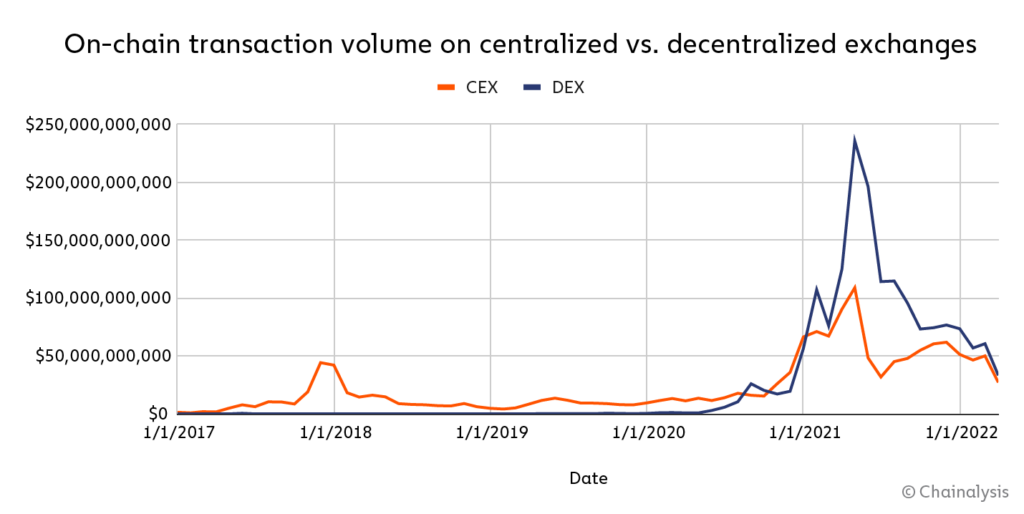

Over the past five years, decentralized exchanges (DEXs) have emerged as a self-custodial, programmatic way for cryptocurrency investors to trade. DEXs allow users to swap between hundreds of trading pairs without an intermediary. And fifteen months ago, these DEXs first eclipsed centralized exchanges (CEXs) in on-chain transaction volume.

While most CEX transactions happen off-chain on centralized databases and captured on their order books to save on transaction fees, every DEX transaction occurs via smart contracts on-chain. For this reason, as well as the rapid growth of DeFi generally, DEXs now have a confident lead in on-chain transaction volume. From April 2021 to April 2022, $175 billion was sent on-chain to CEXs, well below the $224 billion sent to DEXs.

The transaction volumes at centralized and decentralized exchanges are closely correlated with market performance. For example, CEX transaction volume reached an all time high in late 2017 as Bitcoin climbed to its all-time high. Similarly, DEX and CEX transaction volumes alike skyrocketed in 2021 as cryptocurrency prices again multiplied. But with the recent market slump, the amount sent to both exchange types declined, with CEXs proving slightly more resilient than DEXs in current market conditions.

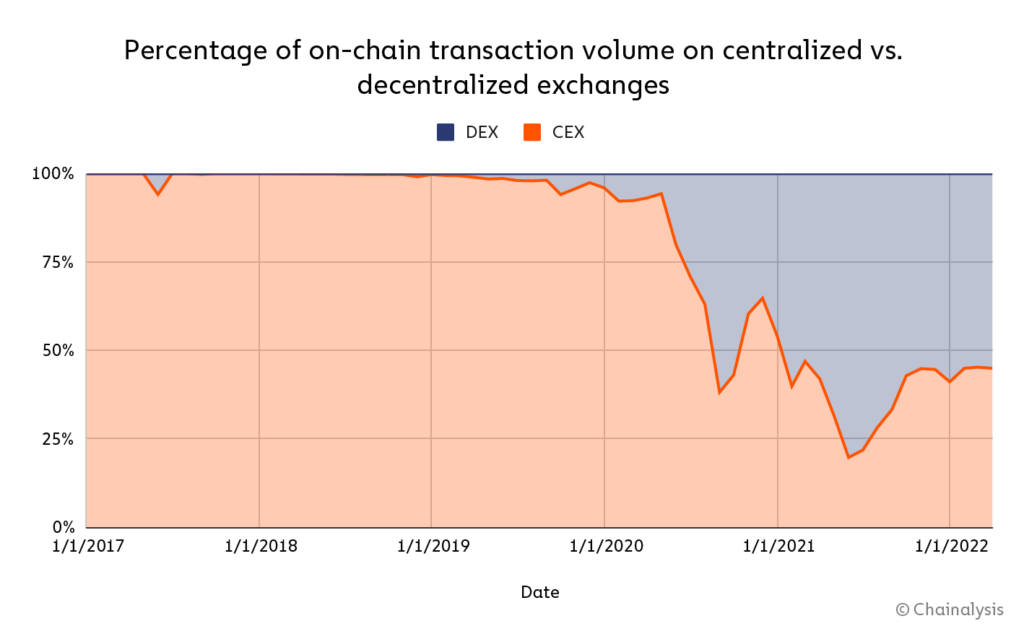

The balance first shifted away from centralized to decentralized exchanges in September 2020, when centralized exchanges supported below 50% of on-chain volume for the first time. DEX dominance then reached its peak in June of 2021; that month, DEXs facilitated more than 80% of on-chain transaction volume. Today, their share of on-chain volume is more evenly split, with 55% happening on DEXs and 45% on CEXs.

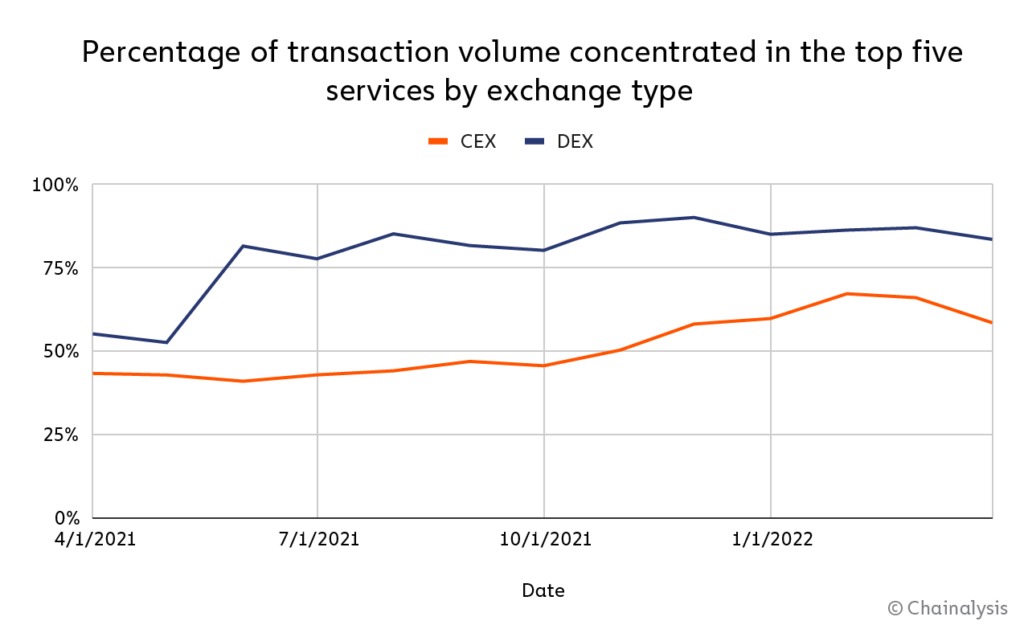

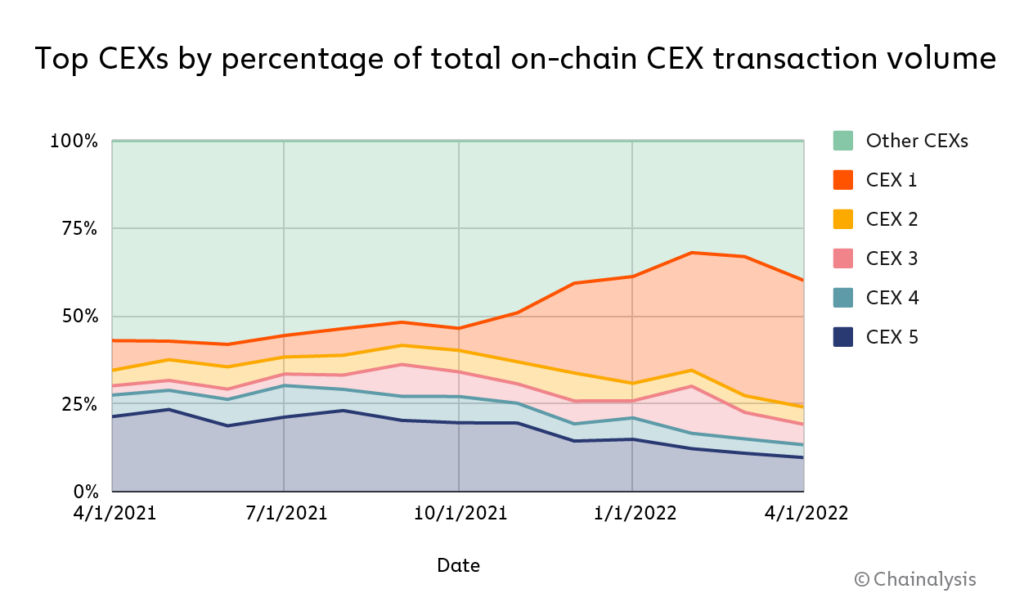

At the service level, the concentration of transaction volume at the top five DEXs is much higher than the concentration of volume at the top five CEXs.

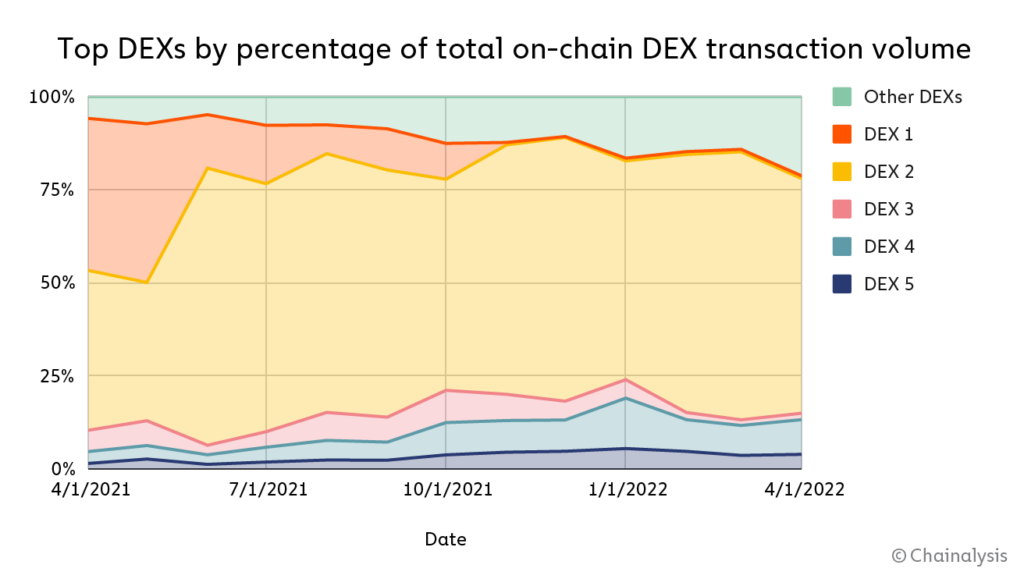

The top five decentralized services currently support roughly 85% of all DEX and aggregated DEX transaction volume during the time period studied. This includes Uniswap, SushiSwap, Curve, dYdX, and the 0x Protocol.

The high concentration of DEX transaction volume is likely a byproduct of DEXs’ recent emergence. Without as much time on the market, fewer DEXs have been able to establish themselves and sustain an active user base. For example, even seemingly established DEXs – like DEX 1 – have seen their users abandon ship en masse during the recent decline in DeFi activity.

Another possible explanation is economies of scale, an important mechanism for DEXs. DEXs with higher liquidity may be able to provide more stabilized pricing for even the biggest market participants, but smaller pools may struggle to do the same without causing considerable price slippage – an unappealing proposition for both consumers and liquidity providers.

By contrast, the top five centralized exchange services – Binance.com, OKX.com, Coinbase.com, Gemini.com, and FTX.com – supported roughly 50% of all on-chain CEX transaction volume during the time period studied. However, it is worth noting again that on-chain CEX volume represents only the flows into and out of CEXs, not the trading volume of their off-chain order books.

Centralized exchanges’ lower concentration may be due to greater competition among CEXs, greater focus on regulatory hurdles within and across jurisdictions, and/or greater variability in how much these services’ users also use personal wallets.

Centralized exchanges’ lower concentration may be due to greater competition among CEXs, greater focus on regulatory hurdles within and across jurisdictions, and/or greater variability in how much these services’ users also use personal wallets.

How much do DEX users earn for providing liquidity?

Many automated market maker (AMM)-style DEXs run on liquidity pools – cryptocurrencies stored in smart contracts that support trading pairs. These pairs, such as ETH⇆USDC and USDT⇆DAI, allow users to swap between almost any cryptocurrency at a fair price and without an intermediary.

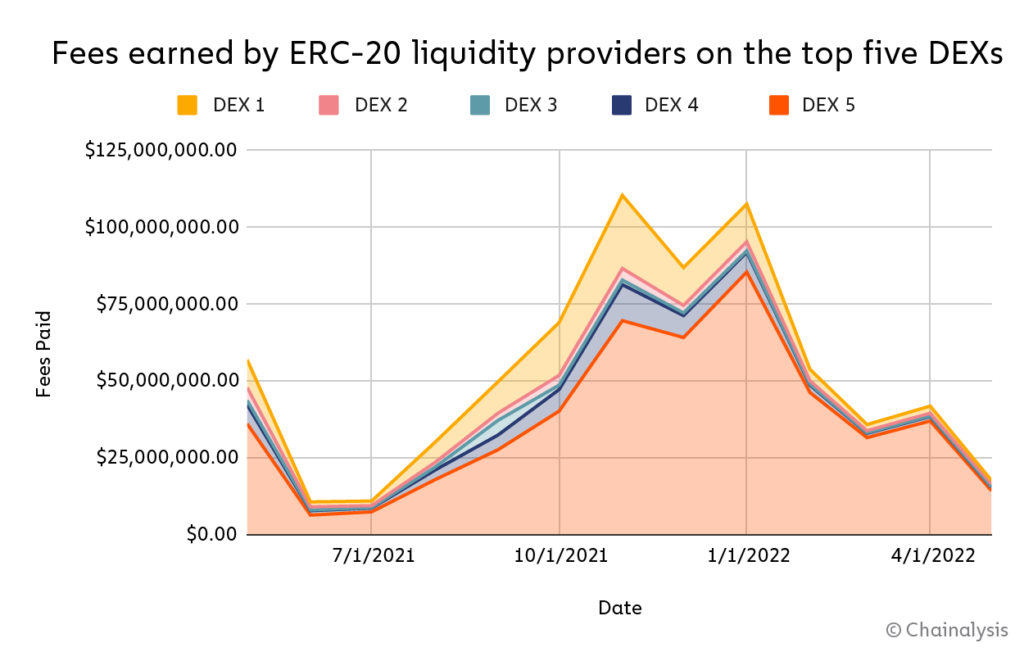

Users who fund these pools are known as liquidity providers or LPs. In exchange for filling these pools with cryptocurrencies, LPs collect transaction fees on any trades that use their liquidity.

How much do LPs earn? To find out, we measured the transaction fees collected by ERC-20 token liquidity providers on the top five DEXs.

The fees earned by LPs are closely tied to DEX transaction volumes. On a monthly basis, fee earnings have fluctuated between $50 and $150 million, a small fraction (0.05% to 0.3%) of the $50 to $300 billion that has flowed through these exchanges during the same period. The recent downturn has impacted both of these elements equally, as fewer transactions means fewer opportunities to collect fees.

Some DEXs also issue governance tokens that may give their holders voting rights over different aspects of the protocol. In some cases, those governance tokens may be traceable on a secondary market.

How are DEX users different from CEX users?

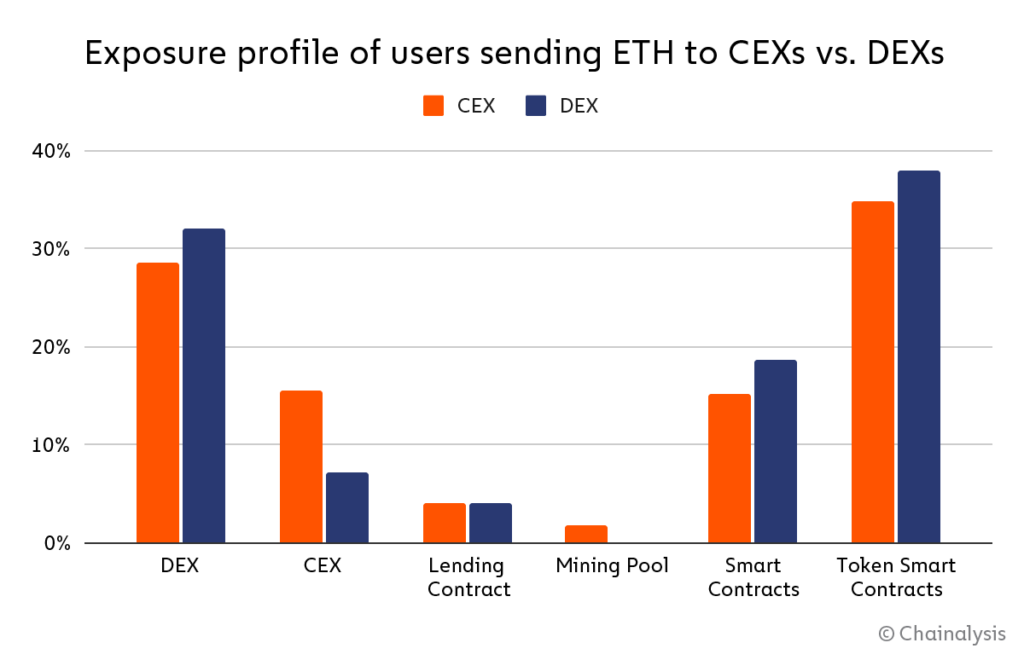

There aren’t any major behavioral differences between the top 10,000 ether (ETH) senders to centralized versus decentralized exchanges, but there are some minor ones.

The biggest difference between the two types of users is in what percentage of their ETH came from a centralized exchange. Just 7% of DEX users’ funds came from a CEX, but 16% of CEX users’ funds came from another CEX. This could reflect decentralized exchange users’ preference for self-custody – both personally and when deciding with whom to transact – over third-party custody.

Will DEXs maintain the lead?

Whether DEXs will ultimately keep their lead in on-chain transaction volume may depend on a number of factors, including:

- whether they can offer lower fees and fairer pricing than their centralized counterparts;

- whether they face more regulatory scrutiny; and

- whether they can shift mainstream attitudes in favor of further automation, disintermediation and self-custody.

As DeFi competition intensifies, it will be interesting to see how CEXs and DEXs converge and differentiate.

Chainalysis does not guarantee or warrant the accuracy, completeness, timeliness, suitability or validity of the information in this report and will not be responsible for any claim attributable to errors, omissions, or other inaccuracies of any part of such material.

This blog is a preview of our State of Web3 Report. Sign up here to download your copy!